CQ WEEKLY

July 16, 2011 – 12:05 p.m.

Political Economy: Dangerous Dance

By John Cranford, CQ Columnist

Congress is currently engaged in a most risky game that’s a little like running blindfolded along the edge of a cliff to escape a bear. And no, this has nothing to do with raising the debt limit or not — except in the most tangential way.

|

||

|

This game involves trying to reduce what most lawmakers and economists agree is an unsustainable budget deficit in the midst of a weak economic recovery, hoping for a long-term benefit without risking a short-term disaster. One false step, and you’re over the edge. Too much hesitation, and you become an ursine lunch.

The relationship between budgetary policy choices and movements in the broader economy is not always clear — and arguments about that relationship are often freighted with ideological baggage. But as Congress moves toward some sort of a deal to raise the debt limit, it seems increasingly likely that a degree of deficit cutting will be part of the package.

The devil, as always, will be in the details of the budget changes. Some lawmakers — mostly conservative Republicans — worry that Congress might prove overly timid in its efforts to throw a rope around a runaway fiscal policy. Because of circumstances and timing, however, the more immediate concern — expressed most often by Democrats — is that Congress might overreach and strangle the economy in the process.

It’s already evident that weak state government finances, coupled with the end of the two-year spend-out of the Obama administration’s economic stimulus program, have contributed to a loss of more than 300,000 state and local government jobs over the past 12 months. Additional spending cuts (forget tax increases, since they are most unlikely as part of any agreement that would pass the House) will only add to the tallies of state and local government job losses, and will increase the economic pain by eliminating both federal worker and private payroll positions.

So, why would President Obama, Senate Majority Leader

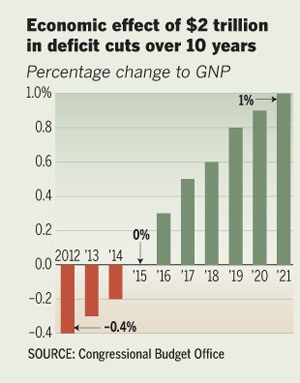

Last week, the Congressional Budget Office released a hypothetical analysis of the macroeconomic effects of a 10-year, $2 trillion deficit reduction plan. As many Democrats fear, the analysis predicts that a phased-in attack of that magnitude on the deficit would reduce overall economic output below its already-weakened state for the first few years it is in effect. Such a step would be particularly problematic because the Federal Reserve has few policy tools at its disposal to offset a fiscal policy contraction.

Still, making allowances for all the caveats and assumptions that CBO attached to this generic analysts, its forecasting model showed a net benefit to the economy over a decade.

Spending and Output

The CBO analysis is based on the expectation that very different factors influence short- and long-term economic output.

For instance, it’s almost axiomatic that a reduction in spending right now will reduce aggregate demand in the economy right now, with the result being a drop in total economic output. Translated: The economy will grow more slowly, and there will be less impetus on the part of companies to hire and reduce the jobless rate. That would be bad, CBO concedes.

Its analysis also assumes that in later years a reduction in borrowing would free up productive capital and labor that in turn would be devoted to expanding overall output and incomes. And that would be good.

Political Economy: Dangerous Dance

Some economists — Kevin Hassett at the American Enterprise Institute, for example — contend that there would be an anticipatory benefit from the presumed future freeing up of capital. That benefit, Hassett says, might — or might not — be sufficient to offset the negative consequences of reduced demand in the near term.

But CBO regards that sort of dynamic scoring as speculative and ignores it. Regardless, its analysis finds a bigger cumulative benefit in the long run and says after 10 years the annual net output of the economy would be a full percentage point larger if the deficit were pared by $2 trillion over that time.

There are cautionary notes, too. Spending reductions that cut deeply into infrastructure or education, for instance, would also risk harming the economy’s future productive capacity — and might limit the overall economic benefit. So, budgetary changes would need to be carefully circumscribed with that in mind. Moreover, timing is also critical, according to CBO. Trying to do too much too soon would risk a bigger short-term squeeze in output.

The bottom line of CBO’s analysis is that cutting the budget isn’t entirely a crapshoot. It promises benefits, but the process involves the gamble that it’s done right. As Tennessee Republican Sen.