CQ WEEKLY

Sept. 3, 2011 – 5:24 p.m.

Political Economy: Bernanke’s Turn

By John Cranford, CQ Columnist

When Standard & Poor’s ripped away the U.S. Treasury’s AAA rating, complaining that a breakdown in the way Congress works threatens the nation’s fiscal solvency, many people shrugged, saying that partisanship and polarization come with the territory. Still others complained that S&P was an upstart outsider that had no business judging the efficacy of Washington’s political machinery.

|

||

|

But now comes

Bernanke is no outsider, despite his academic background and the studied independence of the Fed. He’s been around Washington long enough and has played in high-stakes games. He knows what he’s talking about, and his blast on Aug. 26 was no shot in the dark.

It was delivered at one of the highest-profile monetary policy events of the year, the annual gathering of central bankers and economists from around the world, in the shadow of the Teton Mountains in Wyoming. Whatever the Fed chairman says in those rarefied surroundings tends to be well-amplified.

The question is whether his warning will be heeded any more than those of S&P and others.

“The country would be well-served by a better process for making fiscal decisions,” Bernanke said. And then he zeroed in on congressional behavior, blaming it in part for the nation’s economic malaise, in what had to be a first for any U.S. central banker. “The negotiations that took place over the summer disrupted financial markets and probably the economy as well, and similar events in the future could, over time, seriously jeopardize the willingness of investors around the world to hold U.S. financial assets or to make direct investments in job-creating U.S. businesses,” he said. Ouch.

Bernanke’s willingness to tread on legislative soil and the directness of his language must have surprised many observers. It’s not often that a Fed chairman will speak directly about congressional business — his predecessor Alan Greenspan did so infrequently, and he almost never publicly discussed the way that business is conducted.

But Bernanke has been building to this point for months. During the spring and summer, he repeatedly urged lawmakers not to go to the mat over the debt limit increase. Using the debt limit to leverage an attack on the budget deficit — and particularly to force deep reductions in spending — was both ill-advised (because of the frail state of the recovery) and dangerous (because it risked a default).

So, although he was careful not to point fingers at any specific party or ideological faction in his latest remarks, it doesn’t take a Greenspan translator to see that the Fed chairman has to believe that those who pushed for brinkmanship on the debt limit carry the biggest burden for causing havoc.

Dire Warnings

Beyond his basic criticism that congressional bickering undermines consumer, investor and business confidence, Bernanke offered a direr warning: that the Fed cannot fight this battle on its own. Even if the central bank can continue using monetary policy to support growth, it may not be able to provide much of a lift to the economy. “Most of the economic policies that support robust economic growth in the long run are outside the province of the central bank,” Bernanke said. It couldn’t be clearer that he means it’s now up to Congress to light a fire under the economy.

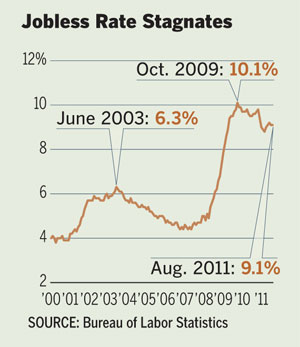

He was clear — even before last week’s lamentable employment report for August, which showed a net gain of zero payroll positions for the month — that jobs must be at the top of the agenda. As he has before, Bernanke cautioned that the nation’s long-term fiscal posture is a serious threat. But, more urgently than in the past, he also warned that lawmakers should not attack the deficit without regard to “the fragility of the current economic recovery.”

Political Economy: Bernanke’s Turn

The chairman’s message that Congress has an obligation to boost employment was oblique only in that he didn’t offer specific policy prescriptions. “To the fullest extent possible, our nation’s tax and spending policies should increase incentives to work and to save, encourage investments in the skills of our workforce, stimulate private capital formation, promote research and development, and provide necessary public infrastructure,” he said.

It’s possible to read the words of this nominally Republican central banker as at least an implied criticism of the Republican fiscal policy agenda, which sees sharply reduced spending and regulation as the only solution to the economy’s woes.

Even in his current mood, Bernanke is unlikely to tell lawmakers exactly what to do. But at the same time, he sounds almost as unhappy with the state of Capitol Hill decision-making as is the public at large. Wonder if anyone up there cares?