CQ WEEKLY

Dec. 3, 2011 – 12:21 p.m.

Political Economy: Lonely at the Top

By John Cranford, CQ Columnist

Oh, to have been a fly on

|

||

|

Best of all, you could have witnessed Bernanke’s response when members of Congress disparaged his stewardship of the economy. You would no longer have to wonder how much he curses.

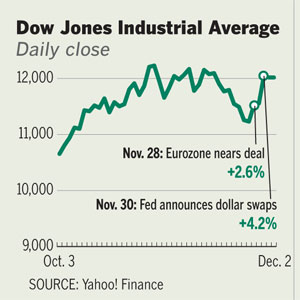

It was really just another week in the office for Bernanke when money markets in Europe threatened to freeze up and block the banks over there from borrowing in dollars to finance their operations. Fearing another Lehman Brothers-like meltdown, Bernanke did what central bankers are supposed to do: He stepped in to keep markets functioning.

The Fed announced Nov. 30 that it will continue swapping dollars for other currencies at favorable rates for the next 15 months. In addition, these swaps — which are transactions with other central banks, not commercial institutions — will be cheaper now than they have been since they began, in 2007.

The whole point is to put dollars in the hands of central bankers in Europe, Canada, Japan and the United Kingdom, which they can make available to their banks as needed.

Dollar liquidity is a crucial matter in finance. And if anyone missed the significance of the swaps announcement, surging stock prices that day amplified the news that, once again, the Fed had for the moment averted a global crisis.

Bernanke’s reward was captured in a critical tweet from Republican Rep.

It’s hard to know where to start deconstructing the multiple misunderstandings in West’s broadside. No, Bernanke doesn’t work for President Obama; the Fed is jealously independent and operates without regard for the political agitations of the government. No, a swap isn’t really a loan; it’s a trade of two things of nominally equal value. No, the Fed doesn’t need to print or borrow dollars for these swaps; it has the money. And if a currency swap between the Fed and, say, the Bank of England truly went sour, there would be no need for a bailout, because, well, the world would be in such a bad spot that it really wouldn’t matter.

Ignorance of finance is no excuse here. There may be reasons to worry about the enormous authority of the Fed. It is very powerful, and it has the means to make or break institutions and investors. There also may be reasons to distrust the Fed’s desire to do its most sensitive business in private — even though under Bernanke the institution is far more transparent than it has ever been.

But there is no reason to gratuitously slam the central bank for performing its most fundamental tasks better than any of its peers. That’s particularly true in the case of the European Central Bank, which lacks the technical, financial and political resources to keep the financial institutions in its own back yard from crumbling.

Not to put too fine a point on it, but the Fed plays hero because it has the wherewithal to do so. No other institution can.

Politically Inclined Potshots

Political Economy: Lonely at the Top

West, of course, is far from alone in trying to make political hay by characterizing the Fed as a bad actor. It’s a parlor game among Republicans these days to see who can take the nastiest shot at Bernanke — presumably because it polls well with a skeptical and worried public. In their debates, the two most prominent GOP presidential candidates, Newt Gingrich and Mitt Romney, call the current Fed chairman a disaster and say he should be replaced.

Gingrich goes so far as to say he would toss Bernanke to the curb, which would not be legal (see the earlier point about the Fed’s independence). “I would fire him tomorrow,” Gingrich said in September. “I think he’s been the most inflationary, dangerous and power-centered chairman of the Fed in the history of the Fed.”

It’s hard to take such rhetoric seriously. Inflation is by almost every measure tame today. Consumer prices actually declined in October, and the year-to-year change in the overall consumer price index is about a third of what it was in the early and mid-1970s, when Arthur Burns, the choice of President Richard Nixon, was chairman of the Fed.

Moreover, Bernanke is the opposite of power mad. He has allowed the seven-member Fed board and the 12 regional Fed bank presidents wide latitude to debate and help guide policy through the most difficult economic period since the Great Depression.

Unlike his predecessor, Alan Greenspan, Bernanke is no man-about-Washington, so he doesn’t have the personal connections to deflect the sticks and stones that were tossed Greenspan’s way only after he left office. Paradoxically, that arms-length relationship with power brokers may have made it easier over the past four years for Bernanke to make the tough calls. Wonder if he sees it that way.