CQ WEEKLY

May 5, 2012 – 1:52 p.m.

Political Economy: Accounting for Risk

By John Cranford, CQ Columnist

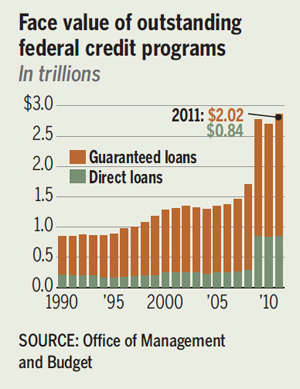

Just maybe, there are a few people in official Washington who would be surprised to learn that the federal government is the nation’s largest lender. Last year, the Bank of Uncle Sam held roughly $2.8 trillion in outstanding direct loans and in guarantees on loans made by private lenders. The government’s portfolio beat out JPMorgan Chase & Co. for the top spot by more than $500 billion in total assets. Bank of America Corp. stood at a more distant No. 3.

|

||

|

No one agency or credit program accounts for the volume of lending, although the Federal Housing Administration carries almost $1.2 trillion in mortgage loan guarantees on its books, and the Department of Education’s college-student loan programs account for more than $700 billion of the outstanding credit.

The total is pumped up by scores of other lending arrangements aimed at assisting farmers, rural development activities, small enterprises and large exporters, to name a few. (Excluded from the total are almost $6 trillion in loans from the four big government-sponsored enterprises — Fannie Mae, Freddie Mac, the Federal Home Loan Banks and the Farm Credit System — because these ostensibly aren’t direct operations of the government.)

However one looks at it, the federal government is deeply engaged in the nation’s credit markets in ways that don’t always come to mind. And the volume of both direct loans and loan guarantees has roughly doubled since 2008.

As a result, government lending is coming under increased scrutiny. In particular, experts are questioning whether Washington budgets properly for the subsidy cost of all these loans.

This is not a new issue. More than two decades ago, Congress enacted the Federal Credit Reform Act, which was the first comprehensive effort to account for the cost of lending programs, which at the time were a pittance compared with today. That law, signed in 1990, requires agencies that make loans and loan guarantees to estimate losses — mostly from borrower defaults — and to budget for those losses using present-value accounting.

That’s where it gets complicated. The 1990 law specifies that losses be adjusted over time to account for the Treasury’s cost of borrowing. Because the federal government is one of the most desirable creditors on the planet, it borrows at the lowest interest rates possible. Critics of the current methodology say it disguises the true risk that the government will incur significant losses.

If those critics are correct, then the measurement of the subsidy cost of federal loans is also too low. They favor moving to a “fair value” accounting method that takes other market-related concerns into consideration. Although current accounting is designed to account for default risks, those who favor the fair-value method say that to properly protect taxpayers, the government ought to consider how private lenders might price these loans.

Is Fair-Value Fair?

Of course, if the budgeted cost of federal lending is pushed higher, that opens the door wider to arguments about whether these loan programs are justified. And it presents the likelihood that they will be pared or that other spending will be reduced to limit the effect of more costly subsidies on the deficit.

The House passed a bill in February — predictably along party lines — that would require the Congressional Budget Office and the Office of Management and Budget to adopt fair-value accounting.

CBO weighed in on this question in a discussion paper in March and appeared to come down on the side of fair-value accounting — without directly calling for a change. Current accounting rules “do not provide a comprehensive measure of what federal credit programs actually cost the government and, by extension, the taxpayer,” the CBO paper’s authors wrote.

Political Economy: Accounting for Risk

If Congress did change the accounting method, then those lending programs that on paper make money for the government — student loans, for instance — would appear to have a cost, CBO said. And those that were shown to add to the deficit would add more.

For its part, OMB is resisting the accounting change — almost certainly because the effect would be to trim the government’s portfolio of loans or cut into other spending. But OMB also raises the quite obvious point that the federal government isn’t really like private lenders. It has no need for a liquid market in these loans, because it doesn’t plan to sell them. And it doesn’t really care whether there is uncertainty about repayment, because the loans are intended to serve a governmental purpose — not to repay investors. At the very least, OMB says, the subject needs closer examination.

The liberal Center for American Progress has joined the debate, issuing a paper last week that reviews two decades of lending under the current accounting methodology. The evidence, according to the Center, is that for the most part government estimates of the subsidy cost of loans have proved to be very close to the actual cost — and, in any case, less than $1 for every $100 in loans.

Accurate budgeting in a time of fiscal stress is no small concern, and there are questions about government lending that no doubt need to be asked. All of that makes a debate about how to budget for federal loans more than a green-eyeshade discussion.